Apple Inc. 1998 Fiscal Year Briefing

Sources: Apple Computer Inc. - 1998 Annual Report

Executive Summary

This document provides a comprehensive analysis of Apple Computer, Inc.’s position at the close of its 1998 fiscal year, based on its Form 10-K filing. The period marked a critical turning point for the company, characterized by a return to profitability after several years of significant losses. This turnaround was the direct result of a multi-year restructuring plan that streamlined operations, simplified product lines, and drastically reduced costs.

The introduction of the iMac in August 1998 proved to be a pivotal event, immediately driving a sequential increase in quarterly sales and signaling renewed consumer and developer interest in the Macintosh platform. However, despite this positive momentum and a full year of profitability, total annual net sales continued their multi-year decline, falling 16% from the previous year.

Strategically, the company made decisive shifts by terminating its Mac OS licensing program, overhauling its distribution channels to focus on fewer partners and direct online sales, and acquiring key technologies through the purchase of NeXT Software, Inc. The primary challenge remains the intense competition from the dominant Microsoft Windows platform, which necessitates that Apple consistently maintain “perceived functional advantages” through innovation. The company’s future success is substantially dependent on its ability to capitalize on the iMac’s success, successfully develop and launch its next-generation operating system, Mac OS X, and navigate significant risks related to its supply chain and global market exposure.

I. Financial Performance and Turnaround Analysis

Fiscal year 1998 represented a dramatic financial reversal for Apple, shifting from substantial losses to sustained profitability. This was achieved through significant operational changes rather than top-line revenue growth, which continued to decline on an annual basis.

Return to Profitability

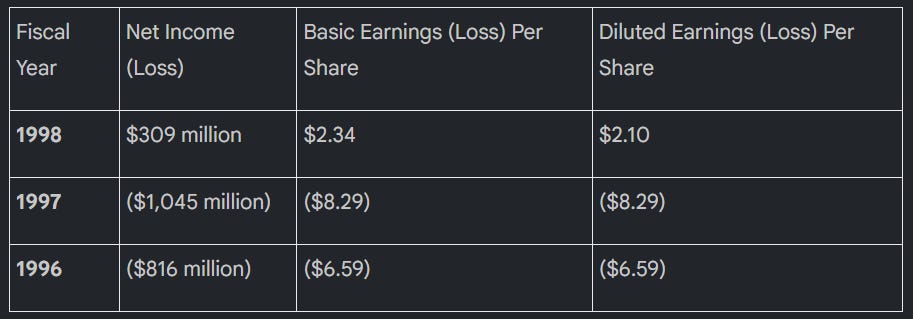

After incurring net losses of over $1 billion in 1997 and $816 million in 1996, the company reported a net income of $309 million in fiscal 1998. Profitability was achieved in all four quarters of the fiscal year.

Sales and Revenue Trends

Despite the return to profitability, net sales decreased by 16% to $5.941 billion in 1998, following a 28% decline in 1997. The annual decline was attributed to:

A $454 million decrease in sales of peripheral products due to discontinuations.

An 11% drop in the average revenue per Macintosh system to $2,095, reflecting aggressive pricing on the Power Macintosh G3 and the introduction of the lower-priced iMac.

A 4% decline in total Macintosh CPU unit sales for the full year.

However, the fourth quarter showed signs of a reversal. The introduction of the iMac spurred an 11% sequential increase in net sales and a 30% sequential increase in Macintosh unit sales compared to the third quarter.

Gross Margin Improvement

Gross margin as a percentage of net sales rose significantly to 25% in 1998, up from 19% in 1997 and 10% in 1996. This improvement was driven by:

A shift in product mix towards higher-margin Power Macintosh G3 systems.

Declining costs for various components, particularly those sourced from Asia.

Improved inventory management from a simplified product line and expanded use of supplier hubs.

Changes to the distribution model, which reduced inventory and related financial exposure.

Operating Expense Reduction

The company’s restructuring plan led to a 32% decline in total operating expenses (excluding special charges) to $1.21 billion in 1998.

Research and Development (R&D): Expenditures were cut by 38% to $303 million (5% of net sales), down from $485 million in 1997 and $604 million in 1996. This was a direct result of focusing R&D on projects “perceived as critical to the Company’s future success.”

Selling, General, and Administrative (SG&A): Expenses fell 29% to $908 million (15% of net sales), driven by headcount reductions and changes to the distribution model.

Selected Financial Data (Five-Year Overview)

(in millions, except per share amounts) | Metric | 1998 | 1997 | 1996 | 1995 | 1994 | | :--- | :--- | :--- | :--- | :--- | :--- | | Net Sales | $5,941 | $7,081 | $9,833 | $11,062 | $9,189 | | Net Income (Loss) | $309 | $(1,045) | $(816) | $424 | $310 | | Diluted Earnings (Loss) Per Share | $2.10 | $(8.29) | $(6.59) | $3.45 | $2.61 | | Cash, cash equivalents, and short-term investments | $2,300 | $1,459 | $1,745 | $952 | $1,258 | | Total Assets | $4,289 | $4,233 | $5,364 | $6,231 | $5,303 | | Shareholders’ Equity | $1,642 | $1,200 | $2,058 | $2,901 | $2,383 |

II. Strategic Restructuring and Operational Overhaul

The 1998 financial turnaround was underpinned by the near-completion of a restructuring plan initiated in 1996. This plan fundamentally altered the company’s cost structure, product strategy, and market approach.

Restructuring Plan (1996-1998)

The plan was “aimed at reducing its cost structure, improving its competitiveness, and restoring sustainable profitability.” Key actions included:

Employee Terminations: Approximately 4,000 of a planned 4,200 full-time employee terminations were completed by the end of fiscal 1998.

Asset Write-Downs: The plan involved writing down land, buildings, and equipment to be sold as operations were downsized and outsourced.

Facility and Contract Cancellations: Certain facility leases and contracts for non-critical projects were terminated.

Financial Impact: The plan resulted in restructuring charges of $179 million in 1996 and $217 million in 1997. As of September 25, 1998, a balance of $31 million remained in accrued restructuring costs for final severance, lease, and contract payments.

Product Line Simplification

A core tenet of the restructuring was to simplify the product line from approximately 15 separate products to three main families, allowing for more focused engineering and marketing efforts.

Core Products: Power Macintosh G3, iMac, and PowerBook G3.

Discontinued Products: The company discontinued its MessagePad and eMate product lines and significantly reduced its imaging (printers) and display (monitors) offerings.

Distribution Channel Transformation

Apple aggressively revised its distribution model to improve efficiency and reduce channel inventory.

Partner Reduction: The company “significantly reduced the number of its distributors, authorized resellers, and national retail channel partners, particularly in the United States.”

Policy Changes: Price protection and stock return privileges for remaining partners were decreased.

Direct Sales: In November 1997, the company began selling products directly to U.S. consumers via its online store.

Termination of Mac OS Licensing

As part of its restructuring, Apple wound down its program of licensing Mac OS to “Clone Vendors.”

In August 1997, the company agreed to acquire certain assets of Power Computing Corporation (PCC), a major clone vendor, for approximately $110 million to terminate its license.

The company stated it “does not plan to extend or reinstate its other Mac OS licensing agreements.”

III. Product and Technology Strategy

Apple’s strategy in 1998 focused on delivering innovative hardware for key markets and laying the groundwork for a next-generation operating system.

Key Hardware Products

iMac: Introduced in August 1998, the iMac was targeted at the education and consumer markets. Its “innovative industrial design, easy internet access and a powerful PowerPC G3 microprocessor” proved immediately successful. In its first partial quarter, sales of the iMac accounted for 278,000 units, or 33% of total Macintosh units shipped.

Power Macintosh G3: This line of high-performance desktops was aimed at business and professional users, focusing on speed, expansion, and networking. G3-powered systems accounted for approximately 98% of all Macintosh units shipped in Q4 1998.

PowerBook G3: This family of portable computers was designed for mobile computing needs.

Operating System Strategy

Mac OS 8.5: Shipped in October 1998, this update delivered new features such as the “Sherlock” search feature and improved network performance.

NeXT Acquisition and Mac OS X: In February 1997, Apple acquired NeXT Software, Inc. for $427 million. The company’s long-term OS strategy is to introduce Mac OS X, which will be based on software technologies from both Apple and NeXT. The report acknowledges significant risks, stating it is “uncertain whether Mac OS X will gain developer support and market acceptance.”

Third-Party Developer Relations

The company reported “renewed interest in the Macintosh platform” from software developers, particularly following the iMac’s introduction.

Over 1,000 new or revised software titles were announced for Macintosh after the iMac unveiling in May 1998.

Microsoft delivered Office 98: Macintosh Edition in early 1998.

An August 1997 agreement with Microsoft ensures that for five years, Microsoft will make future versions of Office and Internet Explorer for the Mac OS. In turn, Apple agreed to bundle Internet Explorer as the default browser.

IV. Market Position and Competitive Landscape

Apple operates in a “highly competitive” personal computer market characterized by aggressive pricing and rapid technological advances.

Market Share: The report explicitly states that “The Mac OS has a minority market share in the personal computer market, which is dominated by makers of computers that run Microsoft operating systems.”

Competitive Pressures: The primary competitive threat comes from the Windows platform. The report notes that “Recent innovations in the Windows platform, including those included in Windows 98 and Windows NT...have added features...that make the differences between the Mac OS and Microsoft’s Windows operating systems less significant.”

Target Markets: The company’s primary customer markets are education, creative, consumer, business, and government. Apple highlights its historical strength as “one of the major suppliers of personal computers for both elementary and secondary school customers, as well as for college and university customers” in the U.S.

V. Key Risks and Forward-Looking Statements

The Form 10-K outlines numerous risks and uncertainties that could affect future results.

Supply Chain Dependence: Key components, including microprocessors and application-specific integrated circuits (ASICs), are sourced from single or limited suppliers. The report identifies IBM Corporation and Motorola, Inc. as the sole suppliers of the PowerPC microprocessor. Any supply interruption could “adversely affect the Company’s business and financial results.”

Global Market Risks: International operations accounted for 45% of net sales in 1998. This exposes the company to risks from foreign currency fluctuations and economic instability. The report specifically notes that weaknesses in Asian markets “have adversely affected and may continue to adversely affect consumer demand.”

Inventory and Manufacturing: The company is increasing its use of third-party outsourcing for manufacturing. While this may lower fixed costs, it also “reduce[s] the direct control the Company has over production and distribution.”

Year 2000 (Y2K) Compliance: Apple has a formal Y2K plan and believes its own branded products are compliant because they use a “long word approach which allows the correct representation of dates up to the year 2040.” However, it notes that the failure of external parties (suppliers, vendors) to resolve their own Y2K issues “could result in a material financial risk to the Company.” Total estimated external spending for the Y2K program is approximately $9.2 million.

Employee Retention: The company experienced “significant voluntary employee turnover” in prior years due to concerns over its prospects. The report acknowledges that the failure to “attract, motivate and retain key employees” could have a significant negative effect.

VI. Corporate and Governance Information

Leadership: As of September 25, 1998, co-founder Steven P. Jobs was serving as interim Chief Executive Officer. The Board of Directors included William V. Campbell, Gareth C. C. Chang, Lawrence J. Ellison, Edgar S. Woolard, Jr., and Jerome B. York.

Headquarters and Employees: The company is headquartered at 1 Infinite Loop, Cupertino, California. As of September 25, 1998, it had 6,658 regular employees and 3,005 temporary or part-time contractors and employees worldwide.

Shareholder Information: The company suspended paying quarterly cash dividends in 1996 and anticipates retaining any future earnings for business operations.

Stock Option Programs: To address employee retention concerns, the company implemented an option exchange program in December 1997. It allowed employees to exchange existing stock options with an exercise price above $13.6875 for new options at that price, but with a new four-year vesting schedule. Approximately 4.7 million options were exchanged under this program.